🎯 TL;DR — Quick Answer

HECM (Home Equity Conversion Mortgage) endorsements rising reflects growing senior demand for reverse mortgage products as Baby Boomers age into the 62+ qualifying threshold. Tim Popp (NMLS #2039627) helps senior homeowners evaluate reverse mortgage options.

⚡ Quick Answer

HECM endorsements rose 16.3% in March, reaching 2,117 loans, indicating growing homeowner confidence in reverse mortgages as a valuable financial tool for retirement. More homeowners are discovering the benefits of these FHA-insured loans to convert home equity into cash. This trend suggests increased interest in utilizing home equity to enhance retirement income.

Are you wondering how to make your retirement savings stretch further, especially with the rising costs we’re all experiencing? Many homeowners like you are looking for smart ways to access the equity built up in their homes to supplement their income and live more comfortably.

Why Are More Homeowners Turning to HECM Loans?

📌 From Tim — In Practice

In my experience, the rising HECM endorsement volume reflects two trends: (1) Baby Boomer demographics — millions hitting age 62 each year; (2) more retirees lacking sufficient retirement savings, looking to home equity for income.

What Exactly is an HECM Loan and How Does It Work?

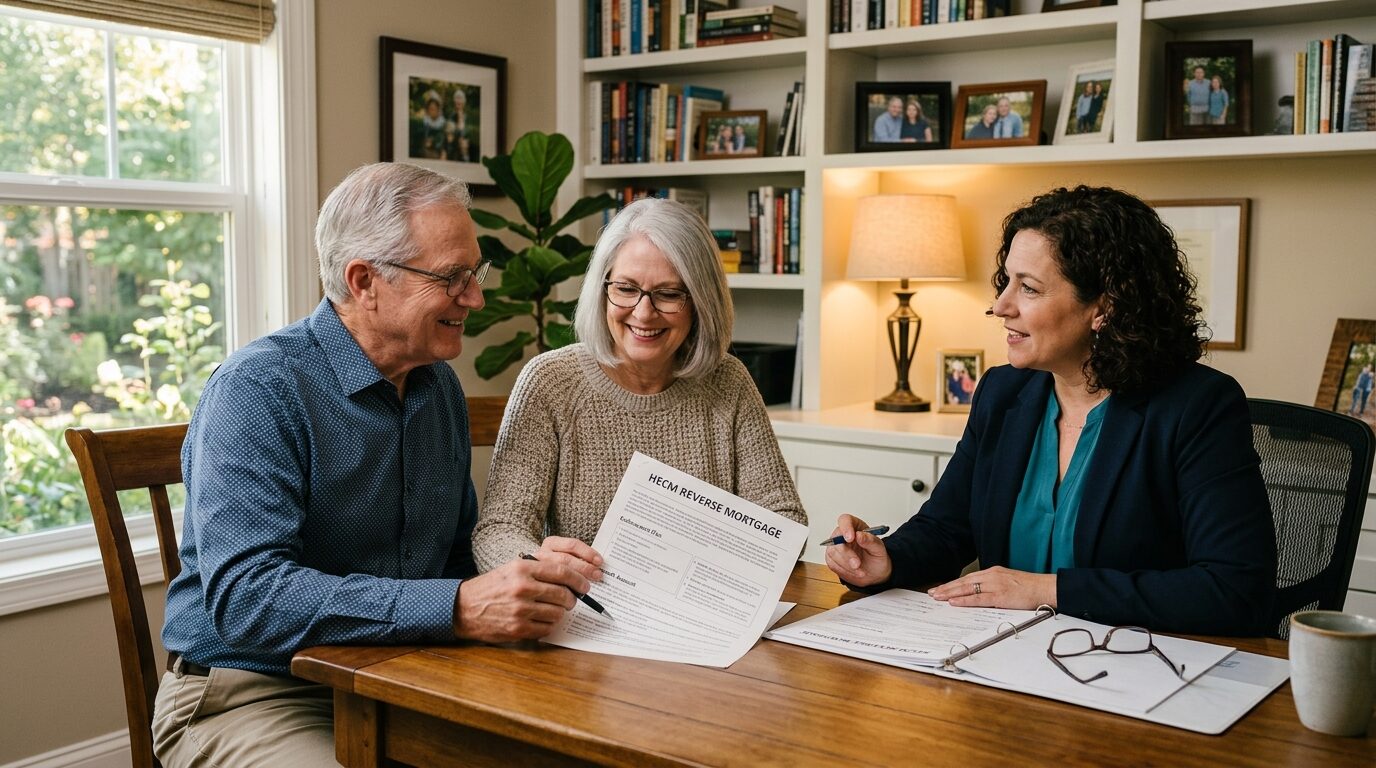

An HECM loan is a type of reverse mortgage specifically insured by the Federal Housing Administration (FHA). It allows homeowners aged 62 and older to convert a portion of their home equity into cash. You can receive this money as a lump sum, regular monthly payments, a line of credit, or a combination of these options. The key difference from a traditional mortgage is that you don’t have to make monthly loan payments as long as you live in the home, pay your property taxes and homeowner’s insurance, and maintain the property. The loan becomes due when the last borrower permanently moves out of the home or passes away. This can be a powerful way to unlock value without the burden of monthly repayments.Understanding Your HECM Options

There are several ways you can receive your HECM funds, each offering different benefits. A lump sum provides immediate access to a significant amount of cash. Regular monthly payments can act like a consistent income stream, supplementing your other retirement resources. A line of credit offers flexibility, allowing you to draw funds as needed, which can be particularly useful for unexpected expenses. Many borrowers find a combination of these options works best for their unique financial situation. For instance, you might take a portion as a lump sum for immediate needs and keep the rest available as a line of credit for future flexibility.Ready to see what you qualify for?

See your options in minutes — we’ll get you a real answer fast.

How Can an HECM Enhance Your Retirement Income?

For many retirees, the concern about outliving their savings is a significant worry. An HECM can provide a reliable source of additional income, easing that anxiety. This can be used to cover day-to-day living expenses, allowing you to maintain your lifestyle without depleting other investments too quickly. Think of it as a way to tap into an asset you already own – your home – to improve your financial security in retirement. It can help you continue to enjoy the comfort and stability of your home while also providing the financial flexibility you need. This can make a real difference in your quality of life.Supplementing Social Security and Pensions

Social Security and pensions are valuable, but they may not always be enough to cover all your retirement needs, especially with inflation. A HECM can bridge that gap, providing extra funds to supplement these existing income sources. This can free you up to spend on things that matter most, whether it’s travel, hobbies, or supporting family. It’s about creating a more robust financial picture for your retirement years. By leveraging your home equity, you can build a more comfortable and secure future.

Accessing Your Home Equity for Various Needs

Your home equity represents a significant portion of your wealth. An HECM allows you to access this value without having to sell your home. This can be incredibly beneficial for a variety of retirement goals and needs. It provides liquidity without requiring you to move. Whether you’re planning for significant medical expenses, looking to make home modifications for aging in place, or simply want to have funds available for emergencies, a HECM can be a strategic solution. It allows you to use your home as a financial resource.Funding Healthcare Expenses

Healthcare costs can be a substantial concern in retirement. A HECM can provide the funds necessary to cover medical bills, prescription costs, in-home care, or other health-related expenses. This can offer peace of mind, knowing you have access to funds when you need them most for your well-being. Having this financial flexibility can make a significant difference in managing your health and ensuring you receive the best possible care. It reduces the stress associated with unexpected medical bills.Making Home Improvements for Comfort and Safety

As we age, our homes may need modifications to improve safety and accessibility. A HECM can provide the funds for essential upgrades like installing grab bars, widening doorways, or adding ramps. These improvements can help you continue to live independently and comfortably in your own home for years to come. Investing in your home’s safety and functionality can also enhance your overall quality of life. It ensures your living environment supports your needs as you get older.Enjoying Your Retirement with Travel and Hobbies

Retirement is a time to enjoy life and pursue passions. A HECM can provide the discretionary funds needed to travel, engage in hobbies, or simply enjoy more leisure activities. This can help you make the most of your retirement years and live a more fulfilling life. It’s about having the freedom to do the things you’ve always wanted to do. Don’t let financial constraints limit your retirement dreams.What Are the Requirements for a HECM Loan?

To be eligible for a HECM loan, there are a few key requirements you’ll need to meet. First and foremost, you must be at least 62 years of age or older. You also must own your home, and it needs to be your principal residence. Additionally, you’ll need to have a significant amount of equity in your home. The amount of equity you have will influence how much you can borrow. It’s also important that your home is in good condition and meets FHA standards.The Importance of Counseling

Before you can finalize a HECM loan, you are required to undergo counseling with an independent, HUD-approved HECM counselor. This is a crucial step designed to ensure you fully understand the HECM loan program, its costs, and its implications. The counselor will explain your options and help you make an informed decision. This counseling session is not about selling you a loan; it’s about educating you. It’s a valuable opportunity to ask questions and get clarity on any aspect of the HECM.Financial Assessment and Home Equity

A financial assessment is conducted to ensure you can continue to meet your ongoing financial obligations, such as paying property taxes, homeowner’s insurance, and maintaining the home. This assessment helps protect both you and the lender. It ensures the loan is a sustainable solution for your retirement. The amount of equity you have in your home is a primary factor in determining how much you can borrow. Generally, homes with more equity will allow for larger loan amounts. This equity is what the HECM loan is based on.Is a HECM Loan Right for You?

Deciding whether a HECM loan is the right choice for your retirement depends on your individual circumstances and financial goals. The recent rise in HECM endorsements suggests many homeowners are finding it to be a valuable tool. It offers a way to access your home’s equity to create a more financially secure and comfortable retirement. It’s a significant decision, and understanding all the pros and cons is essential. For a comprehensive overview, you might find it helpful to read our article on Reverse Mortgage Pros and Cons: Is It Right for You?. Remember, this is about making your retirement work for you.Considerations for Your Retirement Strategy

A HECM loan can be a powerful component of your overall retirement strategy. It can provide a financial safety net, supplement your income, and give you the flexibility to enjoy your retirement years to the fullest. It’s about creating options and reducing financial stress. If you’re curious about the basics of reverse mortgages, our article, What Is a Reverse Mortgage? The Complete Guide, can provide valuable foundational knowledge. Ultimately, the goal is to ensure your retirement is as comfortable and secure as possible.Tax Implications and Other Financial Factors

It’s worth noting that the funds received from a HECM loan are generally not considered taxable income. However, it’s always a good idea to consult with a tax professional for advice specific to your situation. Understanding all the financial nuances is key to making the best decision for your future. You can also explore Are Reverse Mortgage Payments Tax Deductible? for more insights. At timpopploans.com, we are committed to helping homeowners like you understand their options. We believe in empowering you with knowledge so you can make informed decisions about your retirement finances.Talk to Tim about your deal

Whether you’re buying your first rental or your twentieth — straight answers, no runaround.

Tim Popp, NMLS #2039627 | West Capital Lending | Licensed in 36 states + DC. This content is for informational purposes only and does not constitute a commitment to lend or a guarantee of loan approval. All loan programs subject to borrower eligibility, property requirements, and lender terms.

For Different Reader Perspectives

🏠 First-Time Buyer

Quick answer: HECM loans are reverse mortgages for homeowners 62+, not for first-time buyers. As a first-time buyer, you'll be looking at traditional mortgages instead. Focus on understanding conventional, FHA, or VA loans to get started.

From Tim: This one's not on your radar yet—reverse mortgages are for retirees. Let's talk about the loan types that'll actually help you buy your first home and what you'll need to qualify.

💼 Self-Employed

Quick answer: HECM reverse mortgage endorsements jumped 16.3% in March to 2,117 loans. These FHA-insured loans let homeowners 62+ convert home equity into retirement income—no monthly mortgage payments required, and income documentation is typically simpler than traditional mortgages.

From Tim: As a self-employed pro, you know retirement planning looks different without a W2. HECMs can tap your home equity without the income docs that complicate traditional refis—worth exploring if you're 62+.

🎖️ Veteran

Quick answer: HECM reverse mortgage endorsements jumped 16.3% to 2,117 loans in March. While these are for 62+ homeowners, veterans should know VA loans offer 0% down, no PMI, and competitive rates—better options for those still building equity.

From Tim: If you're a vet under 62, focus on VA loan benefits first—no money down beats tapping equity. Once you're retirement age, we can explore all options including HECMs for your situation.

🏘️ Investor

Quick answer: HECM endorsements jumped 16.3% to 2,117 loans in March. While HECMs serve retirees, this signals growing acceptance of equity-based products—relevant as you scale with DSCR loans that focus on rental income, not personal tax returns.

From Tim: This reverse mortgage trend shows equity-based lending is gaining traction. For investors, DSCR products work similarly—your property's cash flow qualifies you, not W-2s. Great for scaling beyond conventional limits.

🏡 Refi / HELOC

Quick answer: HECM reverse mortgages jumped 16% in March, but if you're under 62, consider a HELOC or cash-out refi instead. Both let you tap equity—HELOCs offer flexibility with variable rates, while cash-out refis lock in fixed terms.

From Tim: If you need equity access, we should compare all your options. HELOCs work great for ongoing needs, but a cash-out refi could make sense if we can improve your rate situation too.