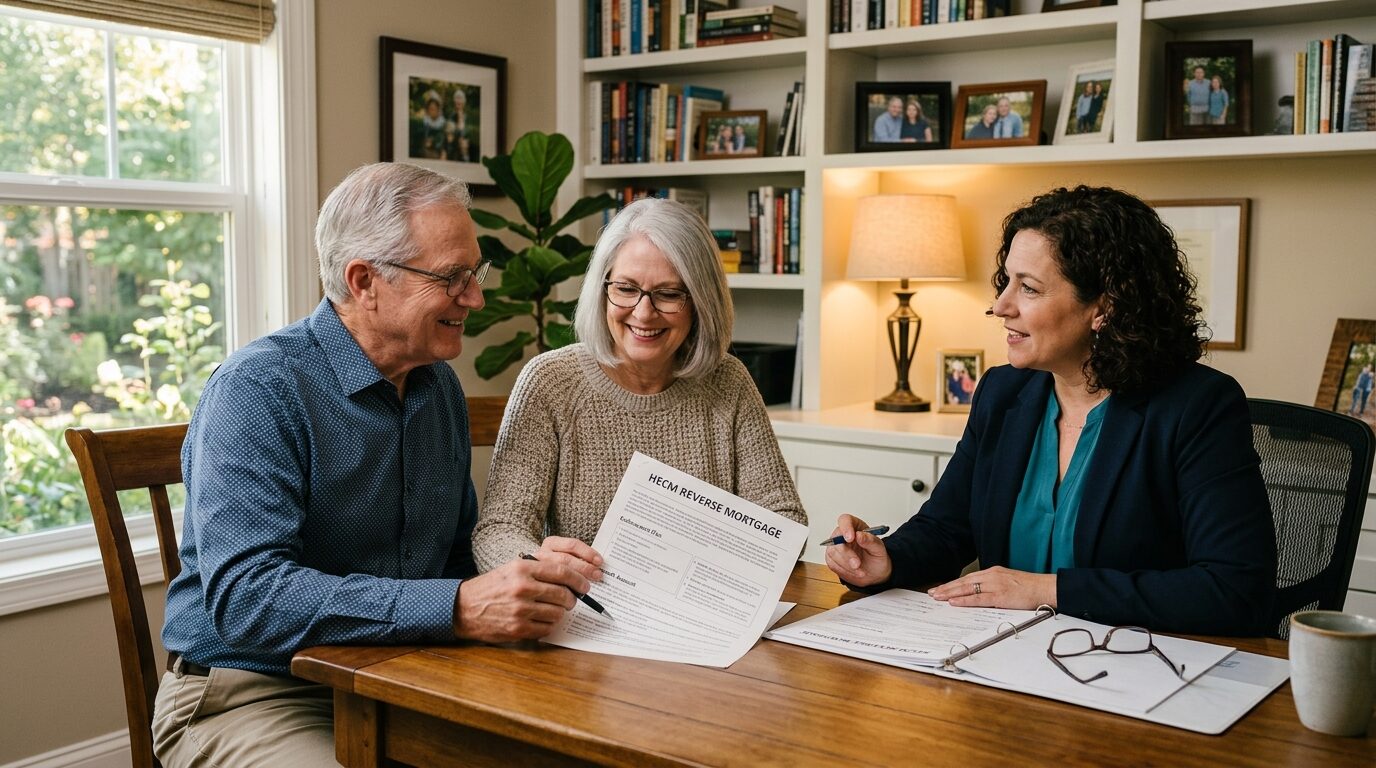

You’ve spent decades building equity. A reverse mortgage lets you access it without selling your home or making monthly payments. Whether you’re supplementing retirement income, funding healthcare, or using the growing line of credit as a strategic financial backstop — this is one of the most misunderstood and underutilized tools in retirement planning.

I’m Tim Popp, Branch Manager at West Capital Lending. I’ll give you an honest assessment of whether a reverse mortgage makes sense for your situation — no pressure, no sales pitch. If it’s not the right fit, I’ll tell you that too. Licensed in 36 states + DC.

Retirement today looks different than it did for our parents. You’ve spent decades building equity in your home, watching its value grow while you raised a family and created a lifetime of memories. As we look toward 2035, your home isn’t just a place to live—it’s becoming a central part of a sustainable retirement strategy. … Read more

You’ve poured your life’s work, memories, and love into building a sanctuary in your home. As you enter your golden years, the last thing you want is a legal technicality threatening your security and peace of mind. For many retirees, a Home Equity Conversion Mortgage (HECM), commonly known as a reverse mortgage, has been an … Read more

Author: Tim Popp, Branch Manager at West Capital Lending. NMLS #2a20007. Licensed in 36 states + DC. You have spent decades building equity in your home, likely watching your property value climb significantly over the last few years. For many retirees, that “brick and mortar” wealth is the largest asset in their portfolio, yet it … Read more

You’ve spent decades building equity in your home, and now that you’ve reached retirement, that equity is likely your largest financial asset. But having a valuable home doesn’t help pay the monthly bills if that wealth is locked behind four walls and a roof, which is why many seniors look for ways to tap into … Read more

You have likely spent decades building equity in your home, viewing it as your most significant asset. Now that you are in your retirement years, you may be wondering how to tap into that wealth without the burden of a traditional monthly mortgage payment. Recent insights from industry leaders suggest that the strategy behind these … Read more

If you’ve spent decades building equity in your home, you’re probably sitting on your most valuable retirement asset. For homeowners along Atlantic Avenue and similar high-value neighborhoods, the home has gone from just a place to live to a real financial tool. You’ve worked hard to maintain your lifestyle, and your home can now provide … Read more

You have dedicated years to building equity in your home, often viewing it as a cornerstone of your retirement security, a flexible financial tool, and a cherished legacy for your heirs. When news breaks about legal disputes involving major reverse mortgage servicers and the freezing of substantial assets, it’s entirely natural to feel a profound … Read more

⚡ Quick Answer HECM endorsements rose 16.3% in March, reaching 2,117 loans, indicating growing homeowner confidence in reverse mortgages as a valuable financial tool for retirement. More homeowners are discovering the benefits of these FHA-insured loans to convert home equity into cash. This trend suggests increased interest in utilizing home equity to enhance retirement income. … Read more

⚡ Quick Answer No, reverse mortgage payments are generally not tax deductible. The funds you receive from a reverse mortgage are considered loan advances, not income, and therefore are not taxable or deductible. However, some associated costs like certain closing costs or mortgage insurance premiums may offer limited deductibility. Retirement often brings a welcome shift … Read more

⚡ Quick Answer A reverse mortgage allows homeowners aged 62 or older to convert a portion of their home equity into cash, without having to sell the home or make monthly mortgage payments. The loan becomes due when the last borrower moves out permanently or passes away. It can be a valuable tool for improving … Read more

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.