Browse 40 year io

Search by keyword, or browse by category.

← Back to magazine view

You are likely looking at a deal right now where the numbers almost work, but the monthly debt service is squeezing your margins tighter than you would like. In the world of real estate investing, cash flow is the lifeblood of your portfolio, and any tool that keeps more money in your pocket each month … Read more

If you’re a real estate investor, you know cash flow is the lifeblood of your business. In a market where traditional 30-year fixed payments can squeeze your margins, the recent enhancement of interest-only offerings is giving investors more breathing room. By extending the loan term to 40 years and including a 10-year interest-only period, these … Read more

Understanding the 40-Year Interest-Only Mortgage for Savvy Investors In the dynamic world of real estate investment, maximizing cash flow and preserving liquidity are paramount. As property values continue to climb and market conditions shift, traditional financing models often fall short of empowering investors to truly scale their portfolios efficiently. If you’ve found yourself navigating the … Read more

Rising property prices and higher borrowing costs are squeezing investors right now. When a traditional 30-year payment eats up your entire rental check, you need something that gives you breathing room—even if it means building equity slower. As a real estate investor, you care about the spread—that margin between what the property makes and what … Read more

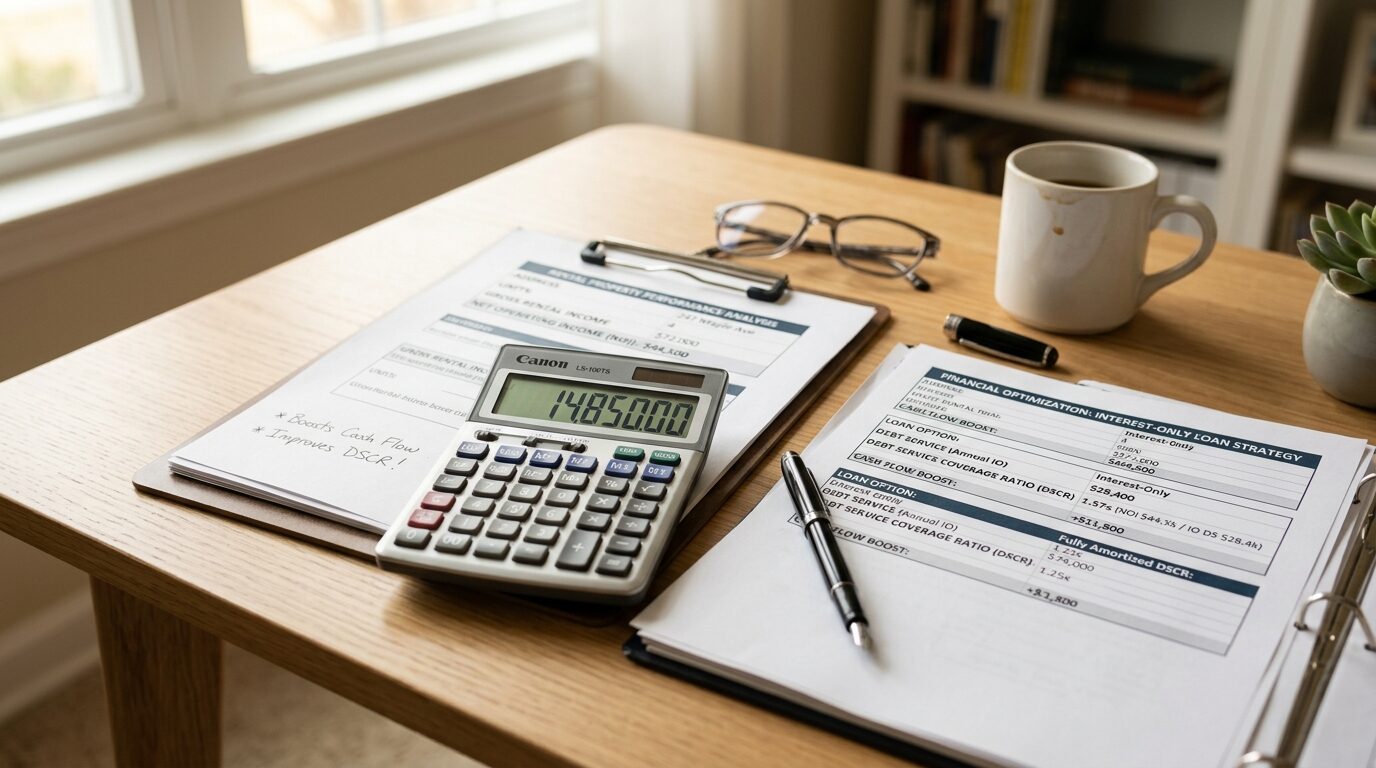

By Tim Popp, Branch Manager at West Capital Lending. NMLS #2a20007. Licensed in 36 states + DC. You have probably spent hours staring at spreadsheets, trying to make the numbers work on a property that is just on the edge of being a “great” deal. In today’s market, where every dollar of cash flow feels … Read more

Scaling a real estate portfolio often feels like a constant balancing act between acquiring new assets and maintaining healthy monthly margins. If you are focused on maximizing your monthly cash flow, you have likely encountered the concept of interest-only financing as a way to keep your overhead low during the early years of an investment. … Read more

As a cash-flow focused real estate investor, you’re always looking for strategies and financing tools that can maximize your monthly income. The allure of a 40-year fixed loan with an initial 10-year interest-only (IO) period is strong, promising exceptionally low payments and significant breathing room for your portfolio. It seems like the ultimate cash flow … Read more

⚡ Quick Answer Nationwide’s extended interest-only offering shows a growing market for investor loans that prioritize cash flow. This means more options, including 40-year fixed loans with initial interest-only periods, for investors seeking lower monthly expenses. These products work well for long-term rental property investors. Nationwide Extends Interest-Only Offering: What This Means for Your Cash … Read more

⚡ Quick Answer A 40-Year Fixed Interest-Only mortgage is a loan allowing borrowers to pay only the interest for a set period, resulting in lower initial monthly payments. This structure can significantly improve cash flow, making it an ideal tool for active real estate investors and DSCR borrowers. It helps optimize property profitability and portfolio … Read more

⚡ Quick Answer Interest-only payments significantly boost your DSCR ratio by reducing the monthly debt service used in the calculation. This allows more of the property’s rental income to count towards covering the loan, potentially turning a “dead deal” into one that meets the typical 1.0+ DSCR requirement. This strategy can unlock properties that wouldn’t … Read more