⚡ Quick Answer Self-employed workers can access home financing through Bank Statement Loans, which verify income using consistent cash flow from bank deposits instead of traditional tax returns. These loans typically require 12-24 months of bank statements, a minimum FICO score generally in the 660-680 range, and down payments often starting around 20-25%. This allows … Read more

⚡ Quick Answer Bank statement loans help self-employed individuals qualify for a mortgage using 12-24 months of bank statements instead of tax returns. Lenders analyze your deposits to determine qualifying income, typically requiring a 10-20% down payment and a minimum FICO score of 660-680. This program offers a clear path to homeownership for entrepreneurs whose … Read more

⚡ Quick Answer Yes, high net worth investors can strategically use DSCR loans to leverage assets and optimize cash flow, despite advice to avoid debt. These loans typically require a 1.0+ DSCR ratio and may allow for portfolio growth without tying up significant capital. This approach often aligns with sophisticated investment strategies more than a … Read more

⚡ Quick Answer No, reverse mortgage payments are generally not tax deductible. The funds you receive from a reverse mortgage are considered loan advances, not income, and therefore are not taxable or deductible. However, some associated costs like certain closing costs or mortgage insurance premiums may offer limited deductibility. Retirement often brings a welcome shift … Read more

⚡ Quick Answer A 40-Year Fixed Interest-Only mortgage is a loan allowing borrowers to pay only the interest for a set period, resulting in lower initial monthly payments. This structure can significantly improve cash flow, making it an ideal tool for active real estate investors and DSCR borrowers. It helps optimize property profitability and portfolio … Read more

⚡ Quick Answer A reverse mortgage allows homeowners aged 62 or older to convert a portion of their home equity into cash, without having to sell the home or make monthly mortgage payments. The loan becomes due when the last borrower moves out permanently or passes away. It can be a valuable tool for improving … Read more

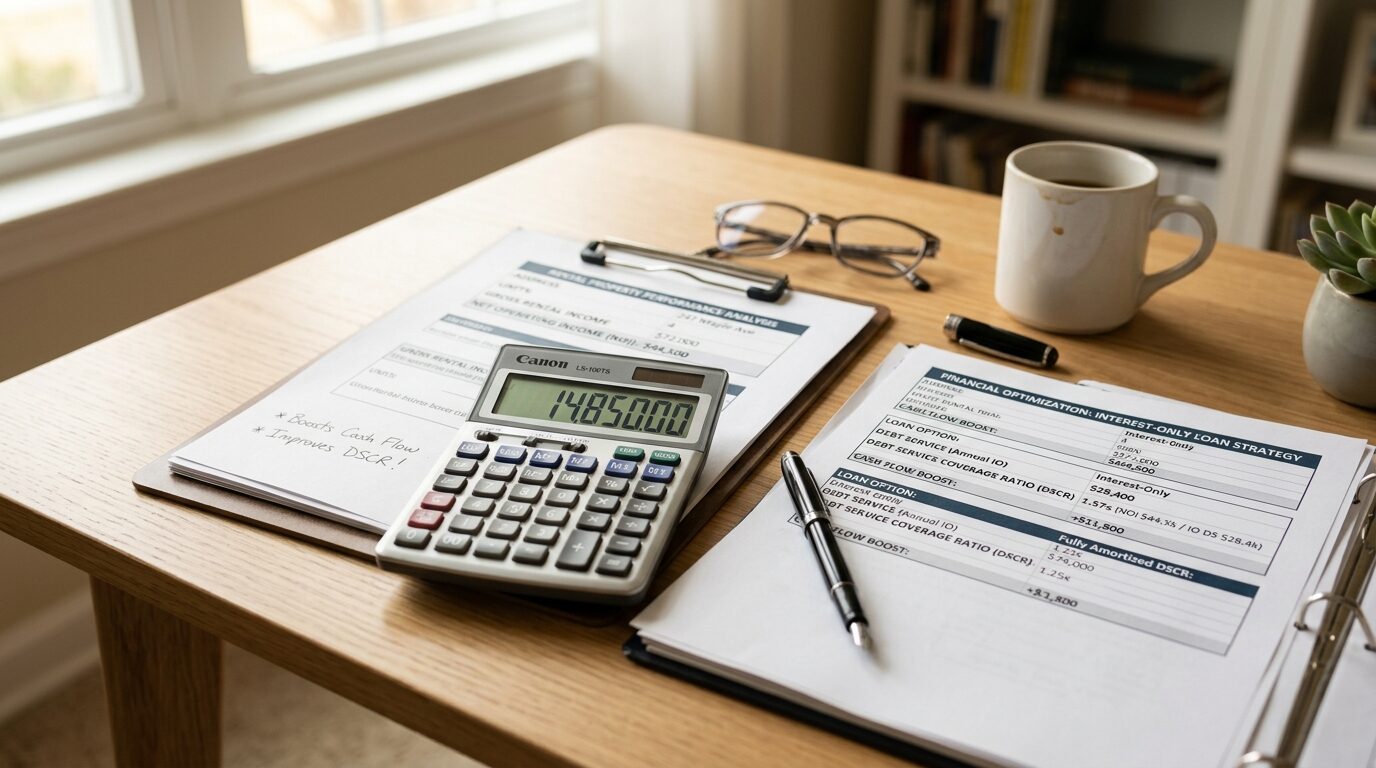

⚡ Quick Answer Interest-only payments significantly boost your DSCR ratio by reducing the monthly debt service used in the calculation. This allows more of the property’s rental income to count towards covering the loan, potentially turning a “dead deal” into one that meets the typical 1.0+ DSCR requirement. This strategy can unlock properties that wouldn’t … Read more

⚡ Quick Answer DSCR loans qualify based on the property’s rental income (typically 1.0+ DSCR ratio). No Ratio loans qualify the borrower through strong credit (660-680+ FICO) and significant equity (20-25% down), without relying on property income. Choose DSCR when property cash flow is strong; use No Ratio when it isn’t. No Ratio vs. DSCR … Read more

⚡ Quick Answer A No Ratio loan is an investor-focused mortgage that doesn’t require debt-to-income (DTI) or debt-service coverage ratio (DSCR) calculations. Instead, it focuses on the property’s value and the borrower’s creditworthiness (typically 660-680+ FICO). This program is ideal for investors with complex income structures or properties that don’t fit conventional loan boxes. What … Read more

⚡ Quick Answer A jumbo loan is a mortgage that exceeds the conforming loan limits set annually by the FHFA. These loans are typically used for high-value properties and generally require excellent credit, substantial reserves, and strong income documentation. What Is a Jumbo Loan? The Complete Guide If you’re shopping for a high-value home — … Read more

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.