Your tax return says one thing. Your bank account says another. If you’re self-employed, run a business, or have income that doesn’t fit in a W-2 box — bank statement loans let you qualify on what you actually earn, not what the IRS sees.

I’m Tim Popp, Branch Manager at West Capital Lending. I’ve helped hundreds of self-employed borrowers and investors get financing when traditional banks said no. Licensed in 36 states + DC.

Tax season brings up the same frustration for most self-employed borrowers. You’re running a successful business, but your CPA has done their job well—minimizing your taxable income through legal deductions and write-offs. Great for April 15th, terrible when you need to tap your home equity. Traditional lenders look at the net income on your tax … Read more

⚡ Quick Answer For self-employed individuals, a “personal loan” often refers to a mortgage. Bank Statement Loans are a common solution, allowing you to qualify for home financing using 12-24 months of bank statements instead of tax returns. This option typically requires a 20-25% down payment and a 660-680 minimum FICO score. As a self-employed … Read more

⚡ Quick Answer Self-employed individuals can qualify for a mortgage using bank statement loans, which assess repayment ability based on 12-24 months of bank deposits instead of tax returns. This specialized product helps business owners with significant tax deductions secure financing. Typically, a minimum FICO score of 660-680 and 20-25% down payment are required. As … Read more

⚡ Quick Answer Self-employed workers can access home financing through Bank Statement Loans, which verify income using consistent cash flow from bank deposits instead of traditional tax returns. These loans typically require 12-24 months of bank statements, a minimum FICO score generally in the 660-680 range, and down payments often starting around 20-25%. This allows … Read more

⚡ Quick Answer Bank statement loans help self-employed individuals qualify for a mortgage using 12-24 months of bank statements instead of tax returns. Lenders analyze your deposits to determine qualifying income, typically requiring a 10-20% down payment and a minimum FICO score of 660-680. This program offers a clear path to homeownership for entrepreneurs whose … Read more

Being self-employed is one of the most rewarding career paths you can take — and one of the most frustrating when it comes to getting a mortgage. You’ve built something real. You’re making more money than most salaried employees in your area. But when you sit down with a conventional lender and they ask for … Read more

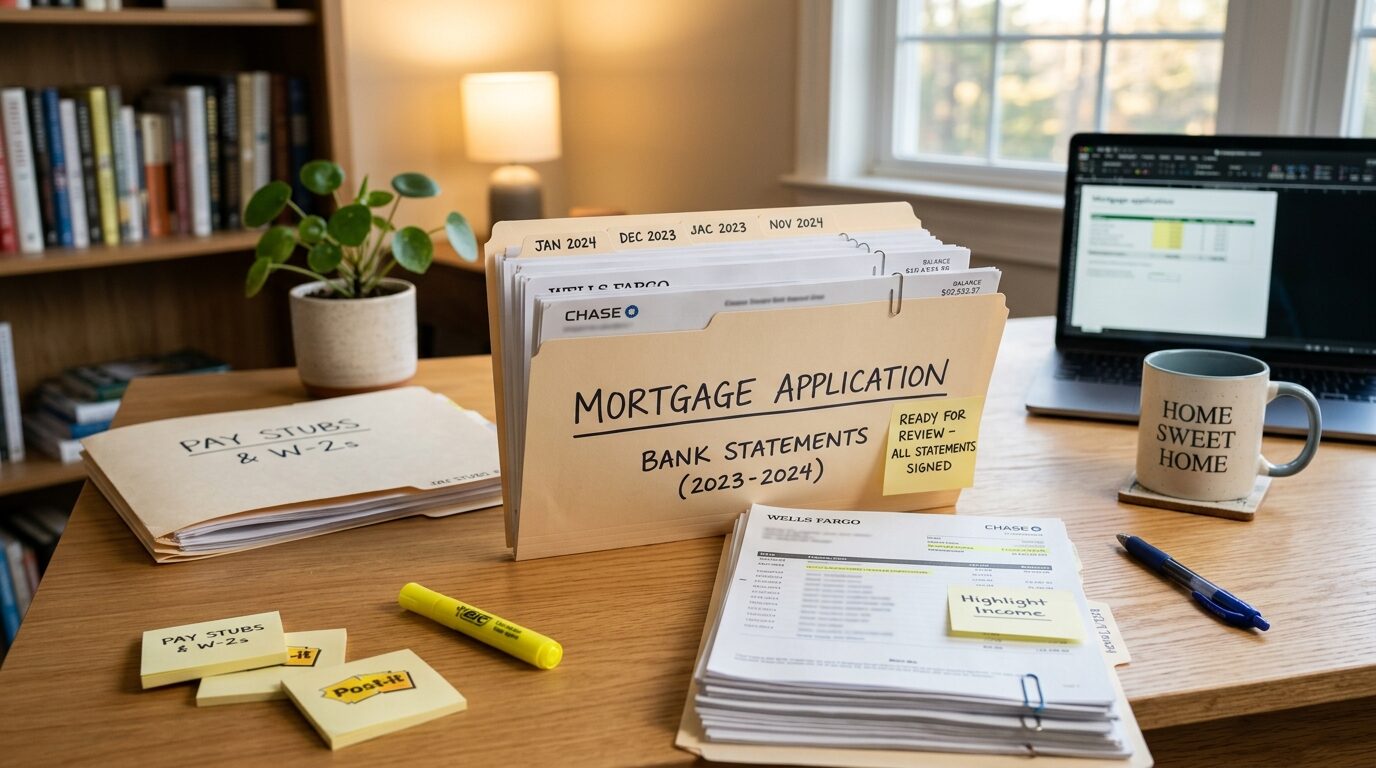

If you’re self-employed and applying for a bank statement loan, the statements you submit are the foundation of your entire application. They replace the W-2s and pay stubs that salaried borrowers provide — which means how you prepare and present them matters more than most borrowers realize. This guide walks through exactly what lenders look … Read more

If you run a business through an LLC, S-Corp, or sole proprietorship, you know your tax return doesn’t tell the whole story. You write off expenses, depreciate assets, and structure income to reduce what you owe the IRS — exactly what your accountant tells you to do. The problem? Traditional mortgage lenders look at that … Read more

One of the first questions self-employed borrowers ask about bank statement loans is: “What kind of rate am I looking at?” It’s a fair question — and the honest answer is that bank statement loan rates run higher than conventional mortgage rates. Why, and what factors decide where your rate lands, helps you figure out … Read more

Real estate investors have a problem. The more properties you own, the more deductions you rack up — depreciation, repair expenses, management fees, mortgage interest. These deductions make sense from a tax perspective, but they systematically suppress the income figure that conventional lenders use to qualify you. You can have substantial rental cash flow and … Read more

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.