Your tax return says one thing. Your bank account says another. If you’re self-employed, run a business, or have income that doesn’t fit in a W-2 box — bank statement loans let you qualify on what you actually earn, not what the IRS sees.

I’m Tim Popp, Branch Manager at West Capital Lending. I’ve helped hundreds of self-employed borrowers and investors get financing when traditional banks said no. Licensed in 36 states + DC.

If you’re self-employed, a freelancer, a business owner, or an investor with complex income — you’ve probably run into the same wall as thousands of other qualified borrowers: you make good money, but your tax returns don’t show it. Traditional mortgage lenders rely almost exclusively on W-2s and tax returns to verify income. For people … Read more

If you’re self-employed and shopping for a mortgage, you’re probably wondering whether you should pursue a conventional loan or look at the bank statement route. It’s not always obvious, and the right answer depends on your financial situation, how you document income, your credit, and what you’re trying to accomplish. This article gives you a … Read more

When you apply for a bank statement loan, one of the first questions your lender will ask is whether you want to use 12 or 24 months of bank statements. It sounds like a simple administrative choice, but the implications for your qualifying income — and your overall loan eligibility — can be significant. Many … Read more

One of the most common questions from self-employed borrowers is simple: What credit score do I need for a bank statement loan? It’s a reasonable question, but the answer is more complex than a single number. Understanding how credit fits into the bank statement loan picture can help you make smarter decisions about when and … Read more

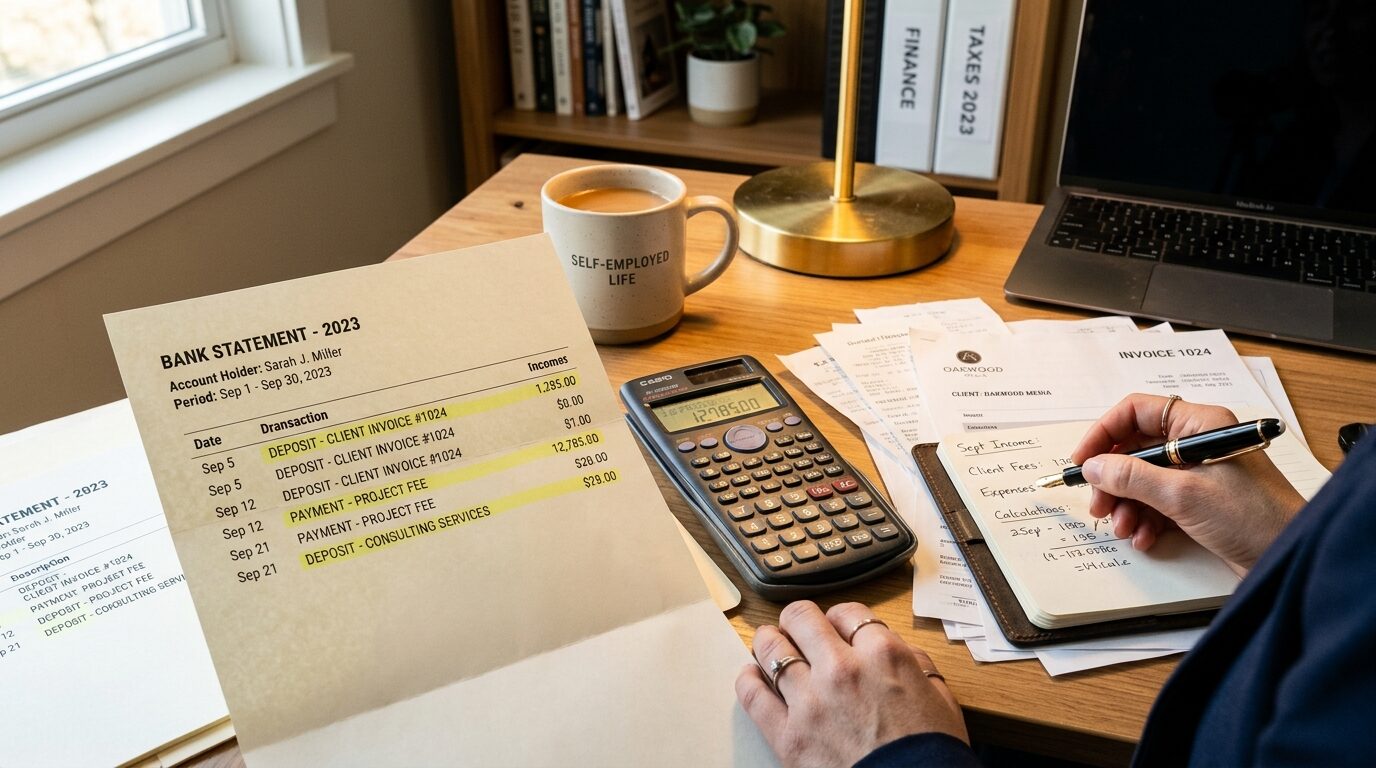

For self-employed borrowers, the income calculation is everything. It determines how much you qualify for, what your debt-to-income ratio looks like, and ultimately whether you get approved. The way bank statement loans calculate income is fundamentally different from conventional mortgages — and understanding the methodology puts you in a much stronger position to navigate the … Read more

Bank statement loans give self-employed borrowers and investors a path to financing that traditional mortgage programs often block. But “alternative documentation” doesn’t mean “no requirements.” These programs have specific qualification criteria — and understanding them before you apply can save you time, set realistic expectations, and help you put together a stronger application. This article … Read more

If you’re self-employed and have equity in your home or investment property, a cash-out refinance can give you access to serious capital. But if your tax returns show less income than you actually make — which happens to most business owners — qualifying through a traditional lender often doesn’t work. A cash-out refinance using a … Read more

One of the most common concerns self-employed borrowers have when exploring bank statement loans is timing. Will it take longer than a conventional loan? What could slow things down? How do you make sure you close on time? These are smart questions to ask upfront. Bank statement loans do have some unique characteristics that can … Read more

The down payment is one of the most important pieces of the mortgage puzzle — and for bank statement loans, the requirements differ meaningfully from conventional financing. If you’re planning to use a bank statement program for a purchase, you need to know upfront how much cash you’ll need at the table, what factors influence … Read more

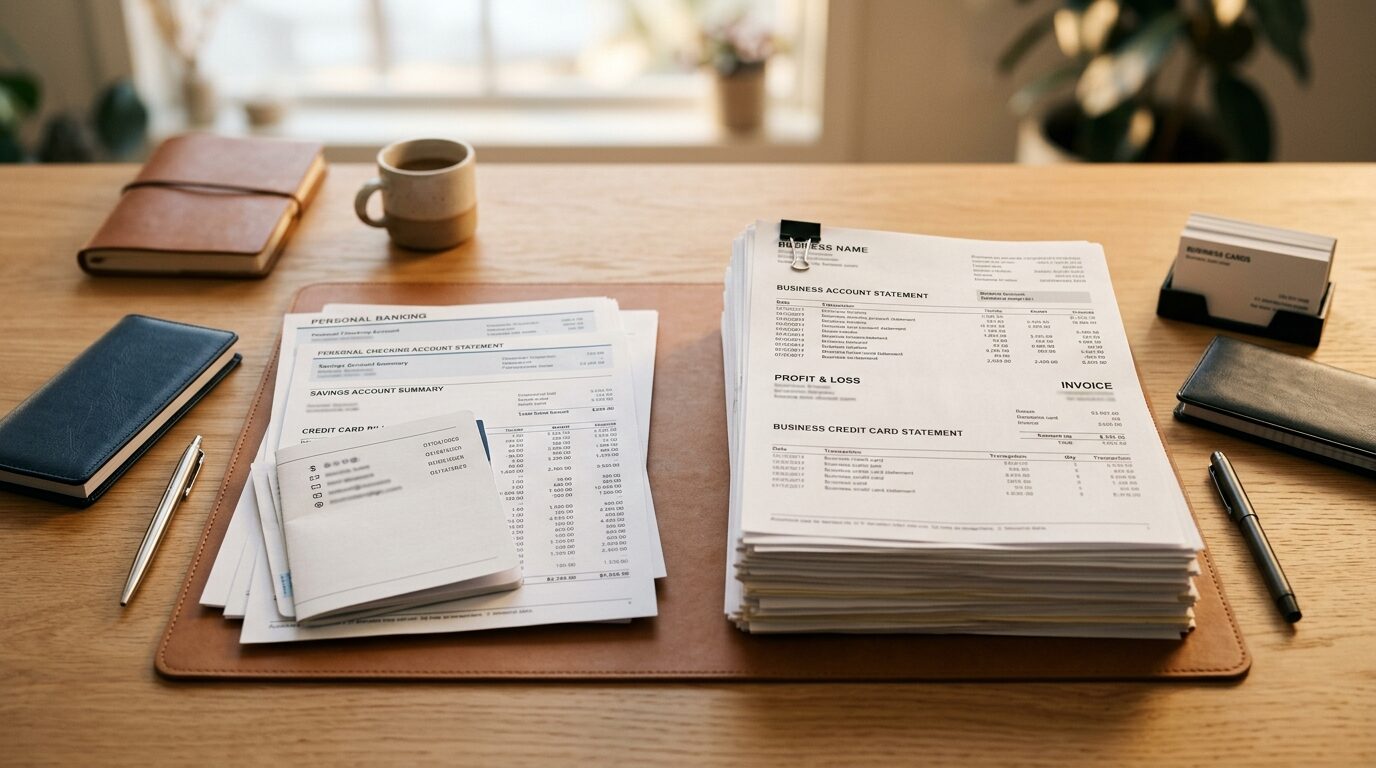

One of the first decisions you’ll face when applying for a bank statement loan is which accounts to use for income documentation — personal, business, or a combination. It might seem like a minor administrative detail, but the choice can significantly affect your qualifying income and, ultimately, your loan approval. Personal and business bank statements … Read more

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.